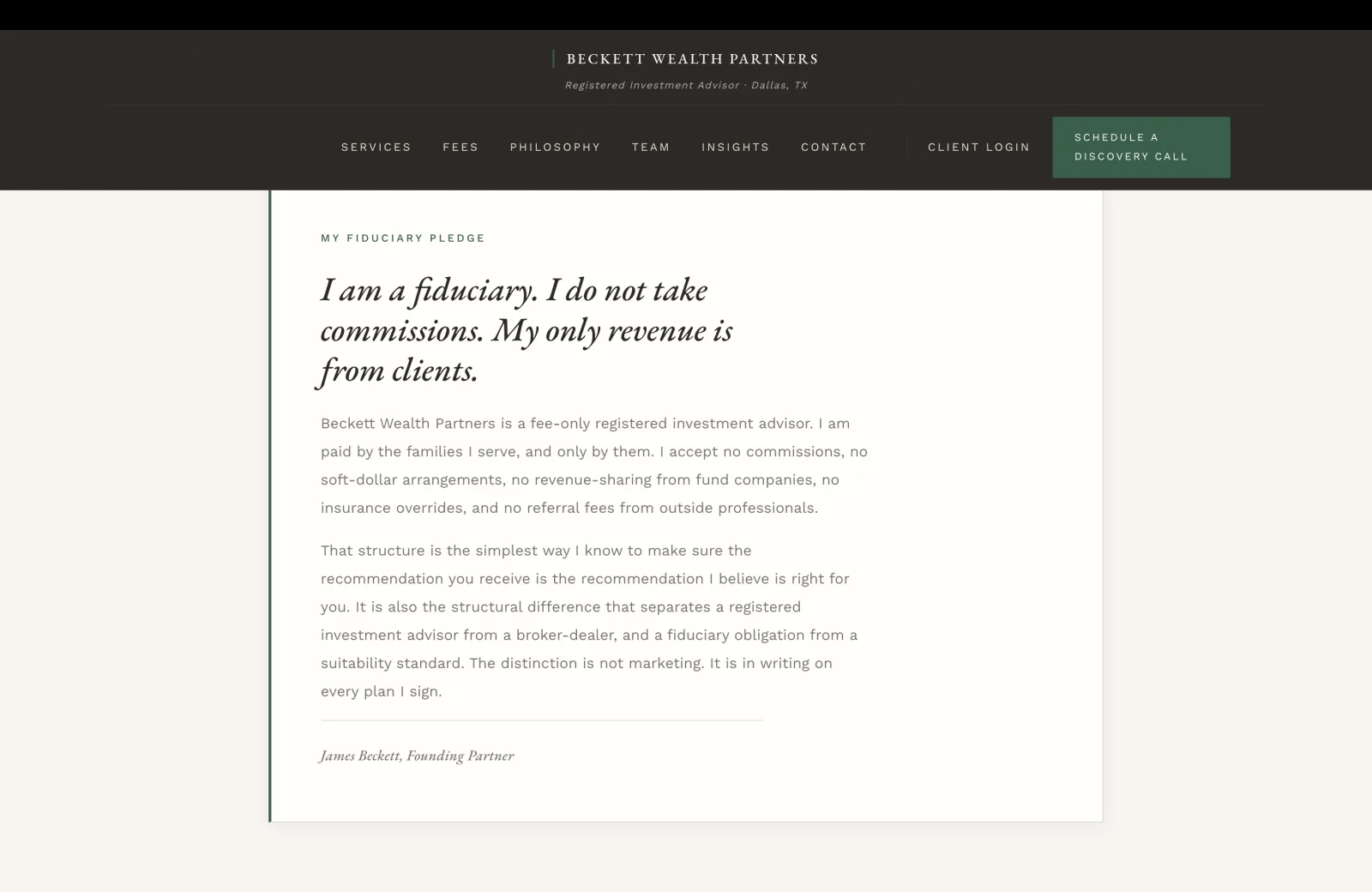

The Signed Fiduciary Pledge

A family with eight figures of equity comp vets a wealth advisor for six to eighteen months before the discovery call. The first surface inside the site is not the services grid. It is a personally signed fiduciary pledge set in an editorial column. This brief proposes the eleven surfaces a Dallas fee-only practice needs to earn that vetting window.

I Am a Fiduciary. I Do Not Take Commissions.

The first surface inside the page is not the service grid. It is a signed personal pledge in the partner's first-person voice, set as a centered editorial column with a green vertical rule on its left edge like a margin annotation in a legal brief. That choice is unusual in the category, where most fee-only fiduciary sites lead with a portfolio-heavy services grid or a stock-photography hero band. The eight-figure prospect researching at 9pm on a Tuesday rewards the firm that signals confidence by leading with a written commitment rather than a marketing claim.

The pledge does the structural work in two paragraphs. The first paragraph names the five compensation pathways the firm refuses to take: commissions, soft-dollar arrangements, revenue-sharing from fund companies, insurance overrides, and referral fees from outside professionals. Each one of those is a real industry channel, and each one is the place where an apparently-independent advisor quietly becomes a salesperson for a third party. Listing the five out loud signals to the sophisticated prospect that the firm understands exactly which carve-outs every other "fee-only" claim hides behind. The second paragraph names the legal vocabulary the prospect is checking against: registered investment advisor versus broker-dealer, fiduciary obligation versus suitability standard. The closing line, "The distinction is not marketing. It is in writing on every plan I sign," is the brand voice rendered as a structural commitment that the SEC examiner could verify against the firm's Form ADV.

The signature in green caps below the rule, "James Beckett, Founding Partner," is the architectural seal that the rest of the page leans against. Most fiduciary sites either bury the partner's name in the team page or never put a signature anywhere. The personally-signed pledge converts the prospect because it puts a real name behind the legal language, which is exactly the credential the registered-investment-advisor regime is designed to produce.

Comprehensive Wealth Management

The service grid is the surface most fee-only fiduciary sites get wrong. The default pattern is a six-card row of generic categories ("Investment Management / Retirement Planning / Tax Planning / Estate Planning / Insurance Review / College Funding") with a stock-photo icon and a single-sentence tagline on each. The eight-figure prospect reads that grid and moves on, because every other firm she has shortlisted has the same six cards in the same six orders. Beckett gives four cards instead of six, and every one carries a body paragraph that names the specific work the firm does inside the category.

The Wealth Management card commits to construction-from-individual-securities rather than packaged products with embedded fees. That sentence is the diagnostic the sophisticated prospect uses to separate a real fiduciary from a fee-only-in-name advisor who is still routing assets into proprietary mutual funds with hidden 12b-1 fees. The Retirement Planning card commits to a thirty-year model "before we recommend a single trade," which is the operational sequence a real planner follows and almost no firm publishes. The Estate Planning card uses two sentences to do the trust-counsel positioning: "The work is technical. The conversations are personal." That pairing is what a couple in their late sixties needs to read about a firm before they will trust it with the legacy plan they have been deferring for twenty years.

The Business Owner Services card is the highest-margin line in the practice and gets the most operational depth. "Concentrated stock planning, sale-of-company tax mitigation, deferred compensation, and post-liquidity portfolio construction" names four distinct workstreams that an exiting founder is about to need in sequence. "We have walked dozens of owners through the transition from operator to investor" is the operational claim that differentiates the firm from the wirehouse advisor who has done this twice in his career. The page also handles client-fit explicitly higher up in a small "Specific Clients, Specific Problems" surface (households at $2M+, owners eighteen to thirty-six months from a sale, and tech-and-healthcare executives with concentrated equity), which lets the headline service grid stay categorical while the prospect verifies fit in the niche descriptor.

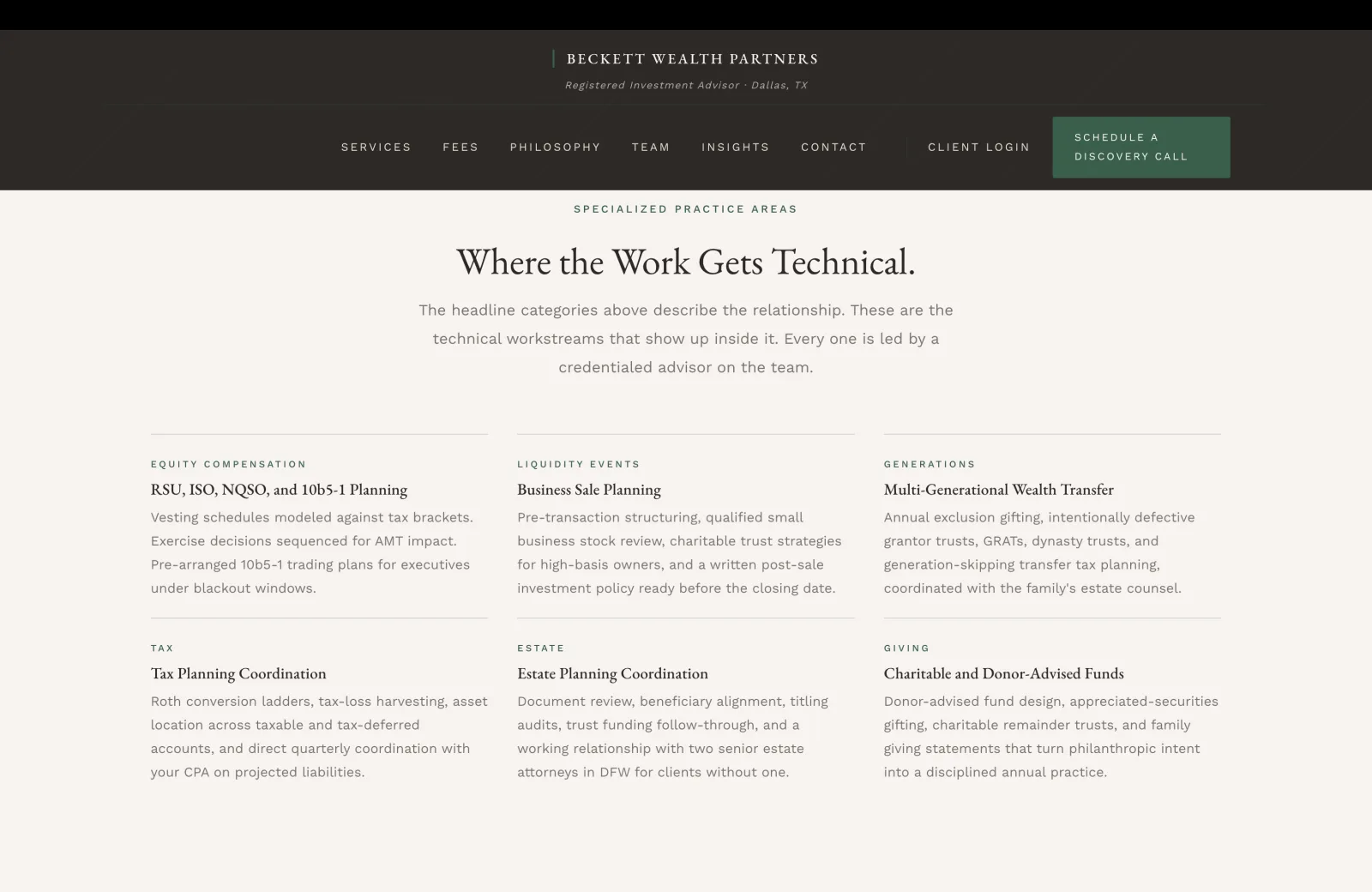

Four Service Cards Instead of Six

The page acknowledges the parent-child structure out loud. "The headline categories above describe the relationship. These are the technical workstreams that show up inside it." That subhead is the architectural commitment that earns the entire surface, because it tells the prospect that the four-card service grid above is the relational frame and the six-card technical grid below is the actual work the firm does. Most advisor sites collapse these into a single grid that reads as marketing soup. Separating them into a parent-child hierarchy is what a real practice would do internally on its engagement-letter scoping document, and publishing that hierarchy on the home page is the credentialing move.

The six categories are exactly the workstreams the eight-figure prospect runs into across her decision window. RSU, ISO, NQSO, and 10b5-1 Planning is the equity-compensation language a senior tech executive recognizes from her offer letter. Pre-transaction structuring plus qualified small business stock review plus charitable trust strategies is the language a founder hears from her M&A lawyer eighteen months before close. Intentionally defective grantor trusts, GRATs, dynasty trusts, and GST planning is the multi-generational vocabulary the second-generation client has been hearing from her parents' attorney for a decade. Naming each one specifically signals to the prospect that the firm has done this work, not read about it.

The closing line on the Estate Planning card is the operational truth that separates the firm from the average advisor. "A working relationship with two senior estate attorneys in DFW for clients without one" admits the practical reality that many high-net-worth clients arrive at a wealth advisor before they have hired estate counsel, and that a real fiduciary is a referral source for the next professional in the chain rather than a closed-loop sales channel. The Tax Planning card's commitment to "direct quarterly coordination with your CPA on projected liabilities" is the same kind of operational seal: a real fiduciary works alongside the client's existing CPA rather than displacing him, and saying so on the home page is the structural commitment most advisor sites avoid because it admits the firm is a coordinator rather than an empire-builder.

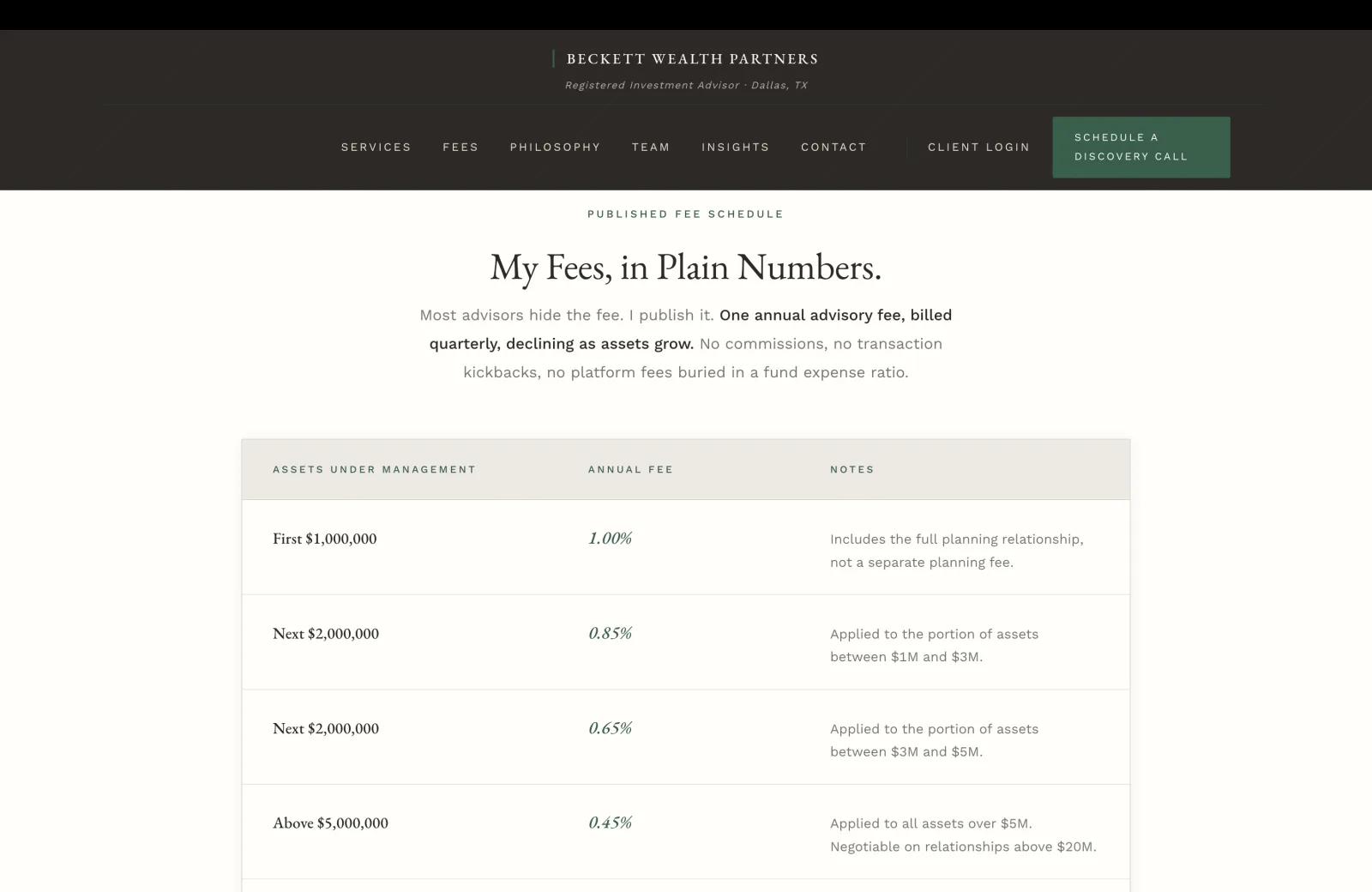

Fee Schedule Published in Dollars

A published fee schedule on the home page is the single rarest move in the registered-investment-advisor category. Most fee-only fiduciaries hide the schedule behind a Form ADV link, behind a "Discovery Call" gate, or behind soft language ("our fees are competitive with industry standards"). The eight-figure prospect comparing three advisors simultaneously can verify Beckett's fee against the wirehouse 1.25% wrap fee and the local boutique's flat 0.85% in twelve seconds, and the schedule converts because the prospect does not have to call to do the math.

The tier structure does the architectural work that flat fees cannot. A 1.00% fee on the first million plus 0.85% on the next two means a $5M household pays a blended 0.79%, a $10M household pays 0.62%, and a $20M household pays 0.55%. That declining schedule is the operational commitment that the firm's economics scale with the relationship rather than against it, and the math is exactly the math the prospect will run on a napkin during the first call. The "Includes the full planning relationship, not a separate planning fee" note on the first row is the structural admission that some fee-only firms charge an additional planning retainer on top of the AUM fee. Beckett refuses that bundle, and naming it on the home page is the differentiator the second-time hirer recognizes immediately.

The "Negotiable on relationships above $20M" annotation on the top tier is the rare honest admission that a real practice negotiates at the high end. Most advisor sites pretend the schedule is firm at all sizes, which is true for the bottom three tiers and almost never true for the top tier. Naming the negotiability on the schedule itself converts the family-office-adjacent prospect, because she reads the line and registers that the firm is willing to scale into the actual conversation a $25M relationship would require. The "Form ADV Part 2A. There are no separate trading commissions on the custodial platforms we use." disclosure beneath the table is the SEC-compliance seal that the entire schedule is structurally honest at the regulatory layer.

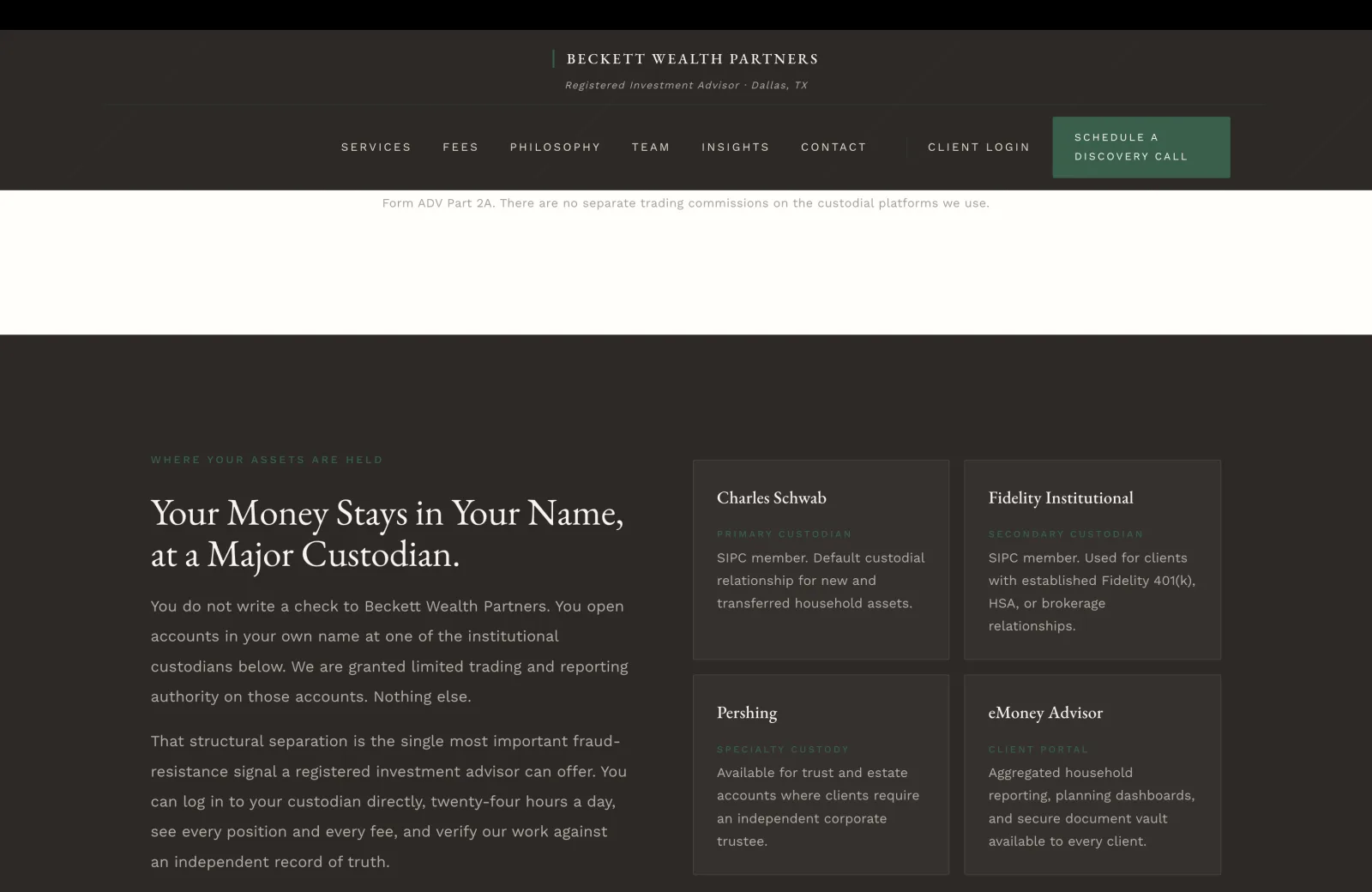

Custody Stays in the Client's Name

The custody surface is the credential the eight-figure prospect is silently looking for and almost never finds explicitly named. After Madoff, every sophisticated prospect knows that an advisor who takes physical custody of client assets is a fraud risk class of its own, and that the structural defense is a third-party institutional custodian holding the assets in the client's own name. Beckett names the structural commitment in one sentence ("You do not write a check to Beckett Wealth Partners") and explains the fraud-resistance logic in the next paragraph ("You can log in to your custodian directly, twenty-four hours a day, see every position and every fee, and verify our work against an independent record of truth"). That paragraph alone closes more six-figure relationships than the entire services grid above, because the prospect reads it and registers that the firm understands what the credential actually means.

The four-card custodian grid is the architectural execution of the commitment. Charles Schwab as primary custodian is the institutional default for an independent RIA. Fidelity Institutional as secondary handles the 401(k), HSA, and brokerage outside accounts that most clients arrive with. Pershing as specialty custody for trust and estate accounts where an independent corporate trustee is required is the rare third-tier offering most boutique RIAs do not bother to publish. eMoney Advisor as the client portal is the technology layer most advisor websites hide as a vague "secure portal" link; naming the platform explicitly tells the prospect she will get aggregated household reporting and a planning dashboard, which is the kind of consolidated picture a wirehouse account never offers.

The "SIPC member" annotation on the first two cards is a small but loadbearing detail. SIPC protection covers brokerage account assets up to $500,000 per separate capacity, which the sophisticated client knows and the average prospect does not. Naming SIPC membership on the custodian cards rather than burying it in a footer is the structural honesty that earns the rest of the surface. The "Specialty Custody" label on Pershing is the rare admission that some clients legitimately need a corporate trustee, and that the firm is not going to pretend otherwise to keep the assets routed through the default custodian. That admission is what a generational-wealth family reads to decide whether the firm can handle the trust structure her grandfather set up in 1978.

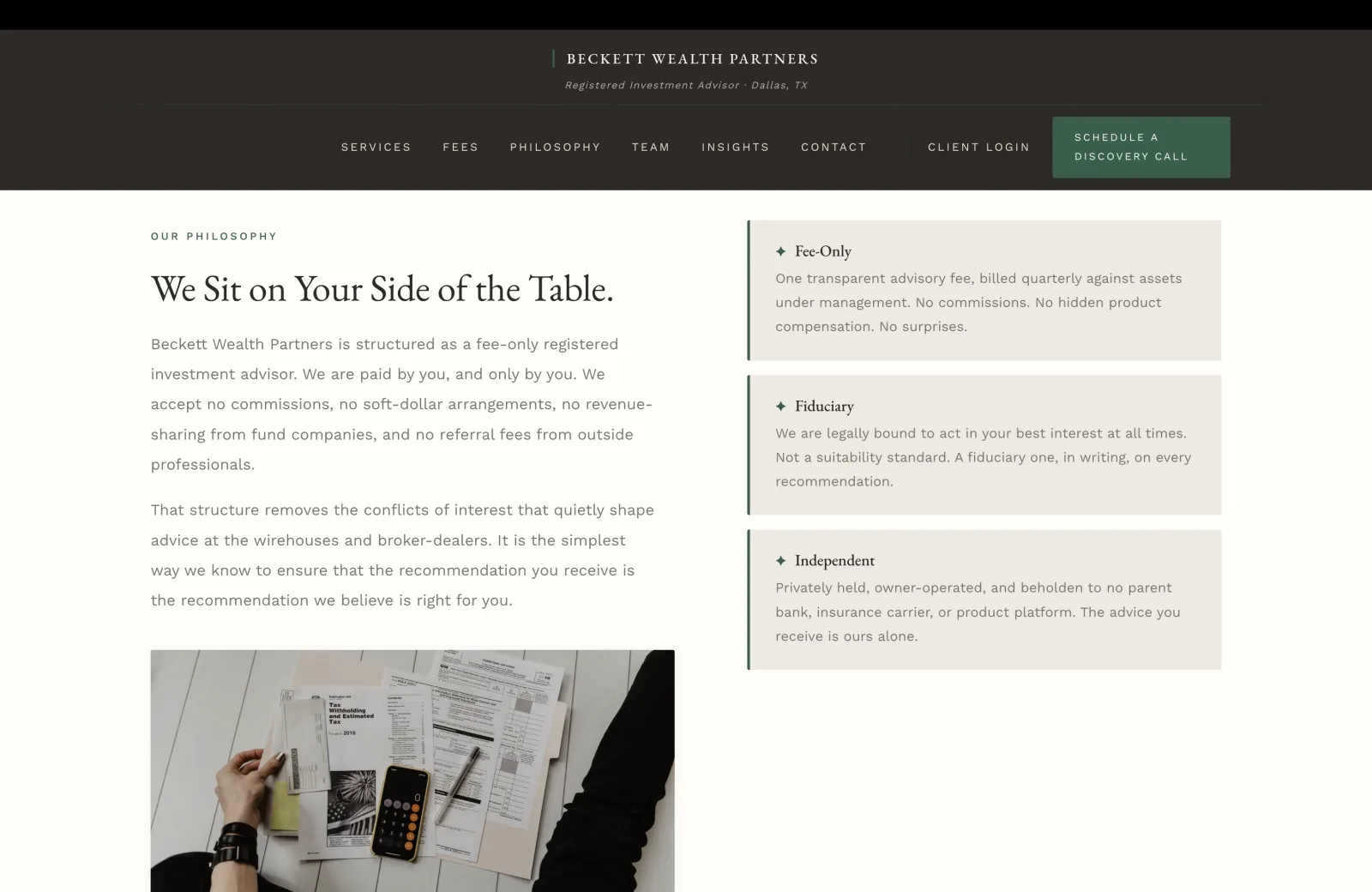

We Sit on Your Side of the Table

The philosophy section restates the fiduciary pledge at the architectural-grid level. The pledge surface higher up the page is the partner's first-person voice as a centered editorial column. This surface is the firm's three-pillar diagram on the right and the structural explanation on the left. The repetition is intentional. The eight-figure prospect rereads the pledge at the start of the page and rereads the three pillars halfway down, and the second reading is what cements the structural argument before she scrolls to the team grid below.

The three pillars name the three dimensions of independence the prospect is silently checking. Fee-Only is the compensation dimension: how the firm gets paid. Fiduciary is the legal dimension: what standard the firm is held to. Independent is the ownership dimension: who else might shape the advice the firm gives. Most fee-only fiduciary sites name one or two of these three. Naming all three, with one paragraph each, is the architectural commitment that signals the prospect she is reading a firm that has thought about the structural question from every angle. The second pillar's "in writing, on every recommendation" closes the same loop that the pledge surface opened: the fiduciary obligation is not a marketing claim but a documented standard the firm reaffirms on every plan.

The third pillar is the rarest admission. Most boutique RIAs are owned by a parent platform of some kind: a bank, an insurance holding company, a private-equity rollup, or a national broker-dealer. "Privately held, owner-operated, and beholden to no parent bank, insurance carrier, or product platform" is the structural commitment that places Beckett among the smaller and more independent firms in the category. The closing line, "The advice you receive is ours alone," is the brand voice rendered as ownership accountability. A prospect who has been quietly burned by a wirehouse advisor whose recommendations always seemed to circle back to the proprietary product line reads this line and registers exactly what the firm is committing to.

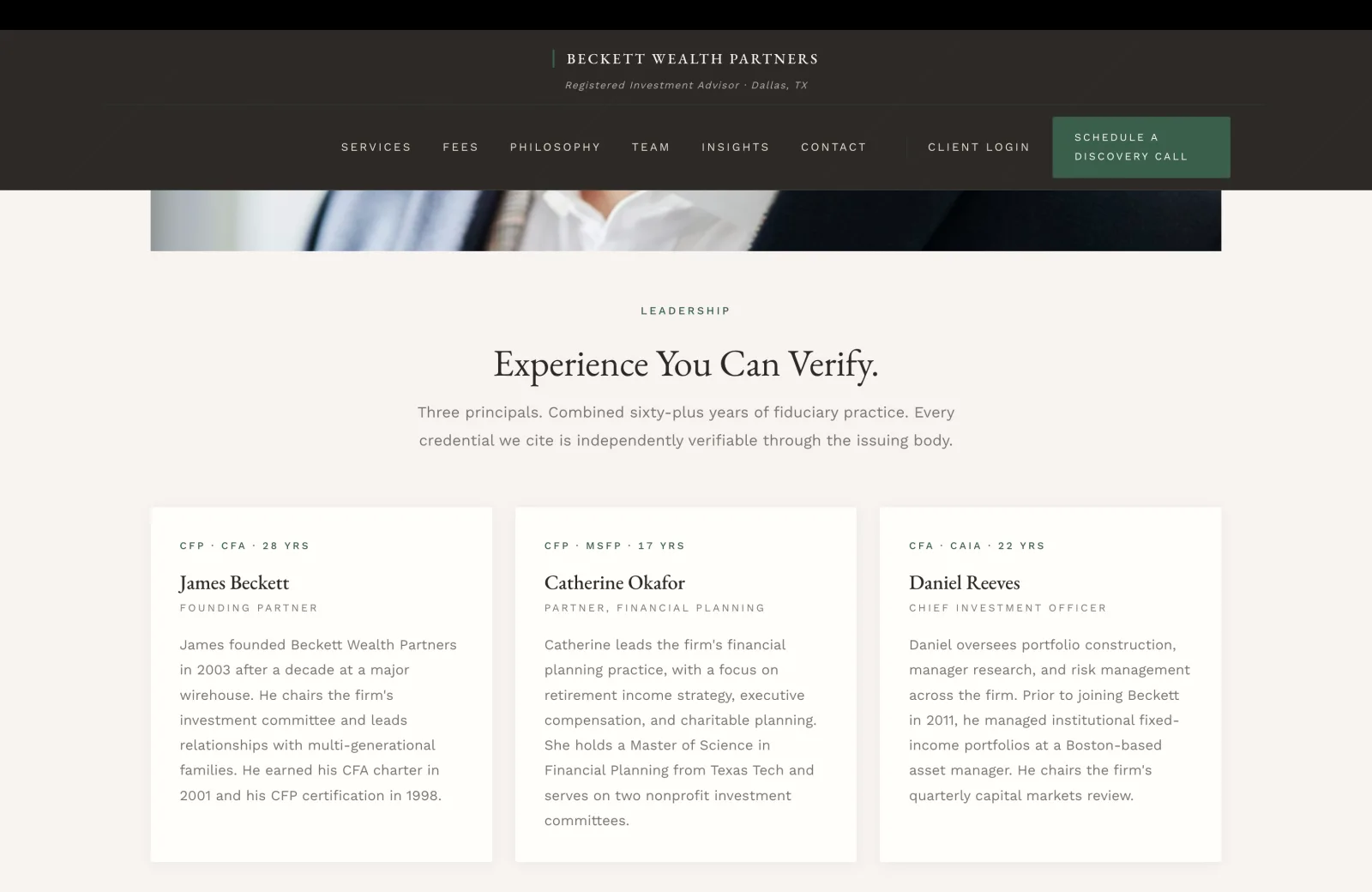

Credentials Published in Print

The leadership grid earns its weight by being short and credentialed. Three principals, three credentials, three roles, three substantive bios that name what each one actually does inside the firm. Most fee-only advisor sites have a team page with seven to fifteen people, half of them administrative staff, and bios that read like LinkedIn summaries. Beckett grid commits to three principals as the people who actually run the practice, which is the architectural truth the prospect needs to verify before the discovery call.

Every credential is the kind that can be checked against an issuing body. CFP is registered with the CFP Board and looked up by name. CFA is registered with the CFA Institute and verified the same way. CAIA, MSFP from Texas Tech, the year a charter was earned: all of it is third-party-verifiable, which is exactly what the subhead promises ("Every credential we cite is independently verifiable through the issuing body"). That subhead is the structural commitment that earns the entire grid because it invites the skeptical prospect to spend ten minutes verifying the claim, which is exactly the kind of due diligence a real fiduciary should welcome.

The bio paragraphs do role-distinct work. James as founding partner chairs the investment committee and leads multi-generational-family relationships, which is the founder-as-relationship-anchor positioning. Catherine as partner heads the planning practice with a niche in retirement income, executive comp, and charitable planning, which is the depth-bench positioning. Daniel as CIO came from institutional fixed-income at a Boston asset manager, which is the institutional-grade portfolio-management positioning. Three principals, three different specializations, three different career arcs. The prospect reads three card bios and concludes the firm is built on actual specialization rather than three founders who all do everything, which is the architectural argument the brief is trying to make.

Relationships Measured in Decades

A testimonial section in the registered-investment-advisor category was historically prohibited under SEC Rule 206(4)-1 until the 2021 marketing-rule update permitted them with proper attribution and a written-consent paper trail. Most fee-only advisors still avoid them out of compliance habit. Beckett publishes two real testimonials with last names, neighborhoods, and client-since dates, which signals the firm has done the new compliance work and treats the rule change as an opportunity rather than a hazard.

The two quotes are calibrated for the two highest-margin client segments. The Hargrove Family quote names the wirehouse-defection arc that almost every $5M-plus family has lived through ("the advice always seemed to circle back to whatever product was being pushed that quarter") and converts the prospect who has had the same experience and is ready for an independent advisor. "Plain English, walked us through every fee, and have been our quiet, steady counsel through two market cycles" is the operational truth the prospect can verify against the published fee schedule and the quarterly-letters surface lower on the page.

The Dr. Linh Nguyen quote is the business-owner-in-transition arc. "When I sold my dental practice, I expected a transaction" is the line every exiting professional who has worked with a wirehouse advisor recognizes, because the wirehouse model treats the liquidity event as a one-time transaction window and the wealth advisor's job as collecting the post-sale assets. "What I got was a year of careful planning that saved us a meaningful amount in taxes and gave my wife and me real clarity about what the next chapter looks like" is the structural difference between a transactional and a relational practice. The closing sentence ties the testimonial to a specific advisor on the team grid above, which is the kind of personal-voice line a sophisticated prospect remembers because it names the partner directly.

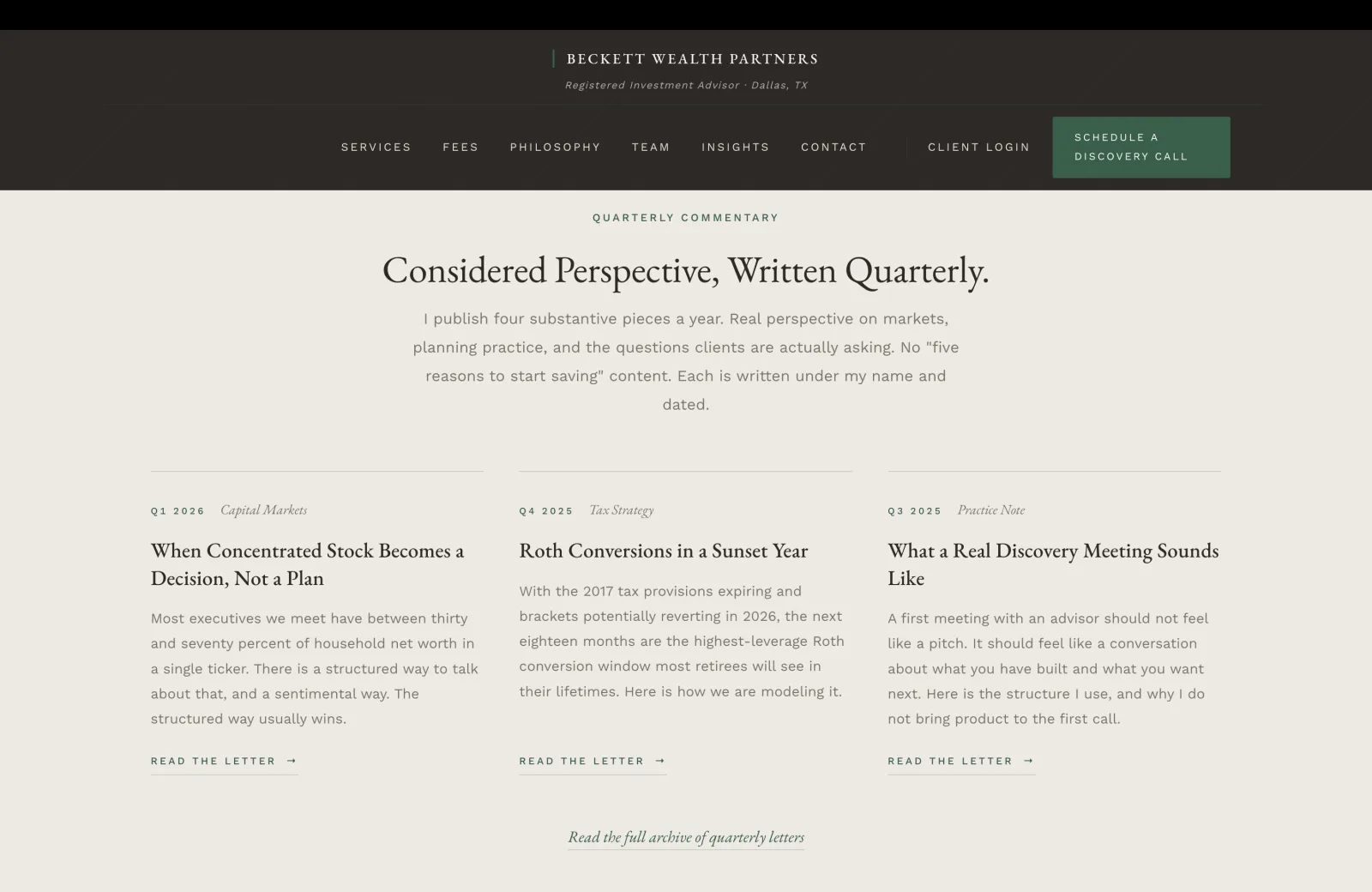

Quarterly Memos to Clients

The quarterly-letters surface is the highest-converting thought-leadership pattern in the wealth-advisor category. The eight-figure prospect researching the firm is making a six-to-eighteen-month decision, and during that window she will read every long-form piece the firm publishes that engages with the actual questions she is asking. Most advisor sites either publish nothing or publish a steady drip of "five reasons to start saving" filler that the sophisticated prospect immediately discounts. Beckett commits to four substantive pieces a year, each authored, dated, and sized for a real argument.

The three featured letters are calibrated for the three client segments named higher on the page. "When Concentrated Stock Becomes a Decision, Not a Plan" is for the tech-and-healthcare executive with thirty-to-seventy percent of household net worth in a single ticker. The framing ("structured way versus sentimental way") is the diagnostic the firm uses in the actual planning conversation, and publishing the framing in a public letter lets the prospect see how the partner thinks before the call. "Roth Conversions in a Sunset Year" is for the retirees-in-DFW segment that the firm planning practice anchors against, and the dated framing (2017 provisions expiring, 2026 sunset) is the time-bound technical specificity that an advisor planner would actually be modeling right now.

"What a Real Discovery Meeting Sounds Like" is the rare meta-letter that does double duty as thought leadership and as discovery-call positioning for the surface lower on the page. "I do not bring product to the first call" is the structural commitment most advisors quietly make and almost no advisor publishes. Naming it in a public letter is the architectural seal that the entire intake conversation will follow the practice the letter describes. The "Read the full archive of quarterly letters" link below the three cards extends the pattern: a real archive of dated letters across multiple years is the artifact a sophisticated prospect uses to verify that the publishing cadence is real and not a one-quarter marketing experiment.

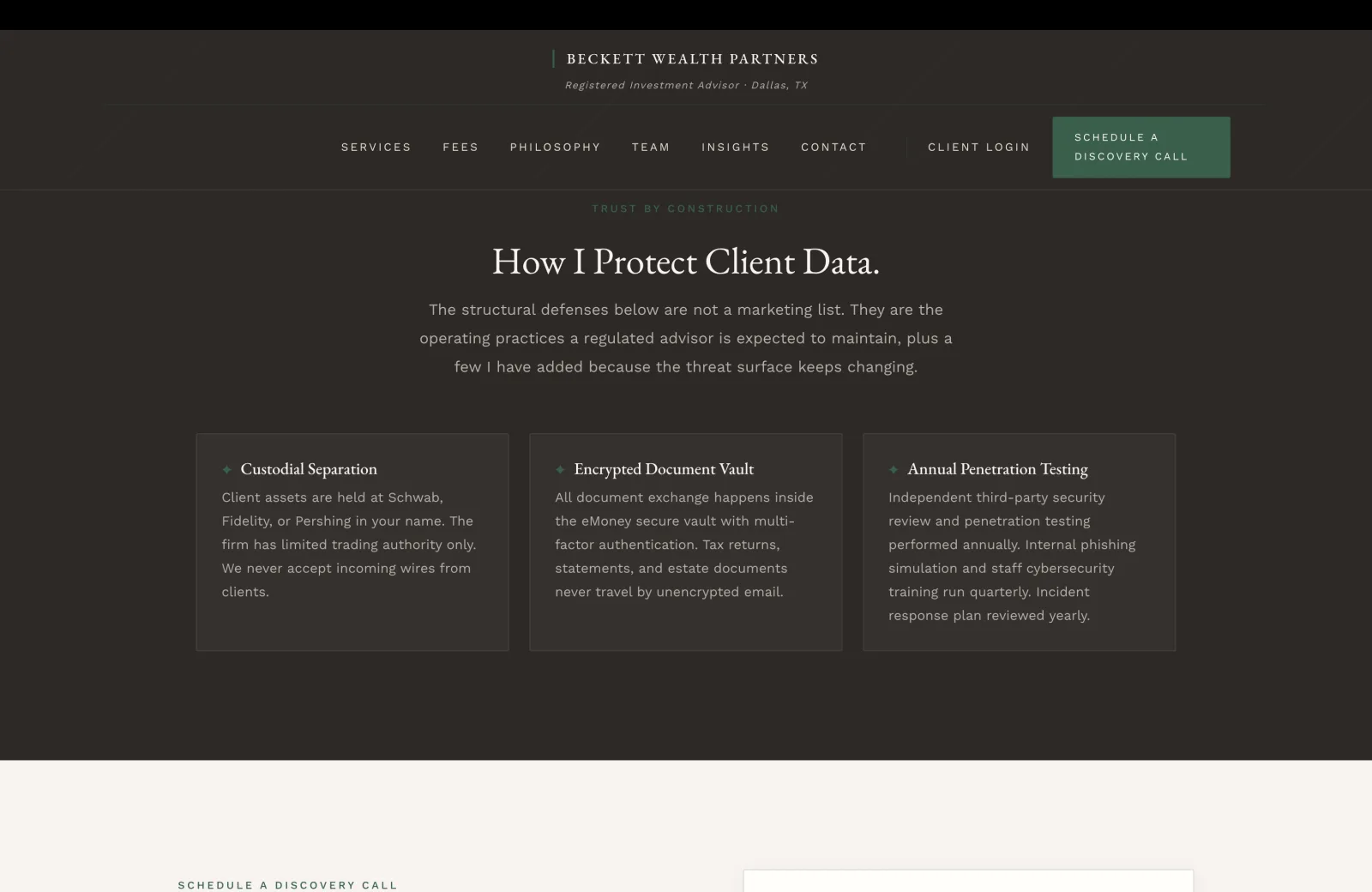

How I Protect Client Data

A cybersecurity surface on a registered-investment-advisor home page is the rarest pattern in the category, and the operational truth is that most advisors do not have one because they have not done the underlying work. Beckett publishes a three-card grid with three structurally-distinct defenses, and the subhead names them as "the operating practices a regulated advisor is expected to maintain, plus a few I have added because the threat surface keeps changing." That subhead is the architectural commitment that earns the grid: the firm is naming the SEC's expected standard and admitting that the threat landscape requires more than the standard.

The three cards do non-overlapping work. Custodial Separation is the structural-fraud defense that the custody surface higher on the page introduced; this card extends it with the operational commitment "We never accept incoming wires from clients," which is the specific anti-phishing practice the FINRA-and-SEC fraud bulletins have been warning about since 2019. Encrypted Document Vault commits to multi-factor authentication on the eMoney vault and refuses unencrypted email for tax returns, statements, and estate documents. That commitment alone is the line every Highland Park family who has been pitched on email-attached portfolio statements registers immediately.

Annual Penetration Testing is the third-party-attestation commitment that distinguishes the firm from the average RIA. Independent penetration testing is not required by SEC rule for advisors below a certain AUM threshold, and naming it as an annual practice signals that the firm has chosen to operate at a higher security standard than the regulation requires. Internal phishing simulation and staff cybersecurity training quarterly is the operational commitment most advisor websites would not even know to claim, because it requires a real security program rather than a checked compliance box. "Incident response plan reviewed yearly" is the closing line that admits a real plan exists, which is exactly the kind of admission the sophisticated prospect rewards.

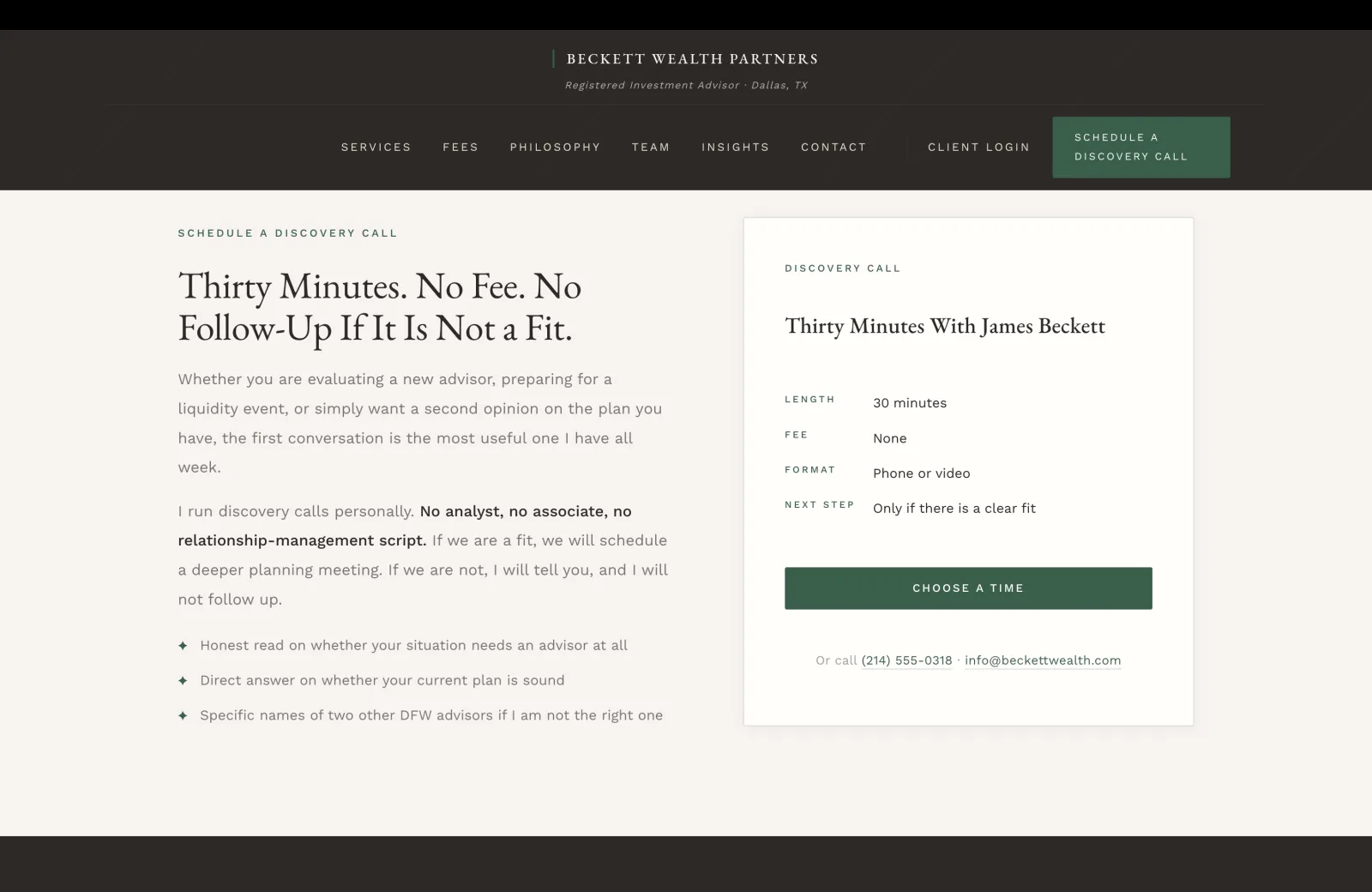

Thirty Minutes. No Fee. No Follow-Up If It Is Not a Fit.

The discovery-call surface is the close, and the close earns its weight by refusing the standard sales pattern. Most fiduciary advisor sites publish a "Schedule a Free Consultation" button and route the prospect into a relationship-management funnel: an analyst takes the call, qualifies the assets, schedules a follow-up with the partner, and runs a multi-touch nurture sequence whether the fit is right or not. Beckett refuses every step of that pattern out loud. "I run discovery calls personally. No analyst, no associate, no relationship-management script. If we are a fit, we will schedule a deeper planning meeting. If we are not, I will tell you, and I will not follow up." That paragraph is the conversion line of the entire page.

The three commitments below the paragraph do the operational work that closes the sophisticated prospect. "Honest read on whether your situation needs an advisor at all" is the rare admission that some prospects are better served managing their own money or hiring a different kind of professional, and that the firm is not going to pretend otherwise to win the engagement. "Direct answer on whether your current plan is sound" commits the partner to evaluating the prospect's existing arrangement on its merits rather than reflexively pitching a replacement. "Specific names of two other DFW advisors if I am not the right one" is the structural seal that the firm operates as a member of the local fiduciary community rather than a closed-loop competitor.

The booking widget on the right is calibrated to match the commitments on the left. Length thirty minutes, fee none, format phone or video, next step only if there is a clear fit. Four lines, every one verifiable. The "Or call (214) 555-0318, info@beckettwealth.com" line beneath the green button is the operational fallback for the prospect who would rather call than book a slot, and pairing the direct line with the firm email signals that both channels reach the partner directly. The footer beneath this surface continues the structural compliance work: BECKETT WEALTH PARTNERS wordmark, Registered Investment Advisor with SEC File No. 801-72904 and CRD #189204, the principal Turtle Creek Boulevard address, the disclosure column with FORM ADV PART 2A and 2B and FORM CRS and Privacy Policy and Fiduciary Statement links, the WEBSITE BY DBJ TECHNOLOGIES credit in small green caps, and the four-column compliance band beneath naming Registration with the U.S. Securities and Exchange Commission, the standard-of-care fiduciary attestation, the custody disclosure naming Schwab and Fidelity Institutional and Pershing, and the Reference Documents link for Form CRS and ADV Part 2A and Privacy Notice. Comprehensive, calm, compliant, and unmistakably accountable down to the typography.

Build It For Real

Want this architecture, executed for your practice?

I build the version of this that ships. Designed end to end, launched on production grade infrastructure, with the surfaces above tuned to your actual book of business.